You worked hard for your degree—but now it feels like your degree is working against you. Every payment reminder, every rising interest rate, every financial “success story” on social media can feel like salt on an open wound and cause depression.

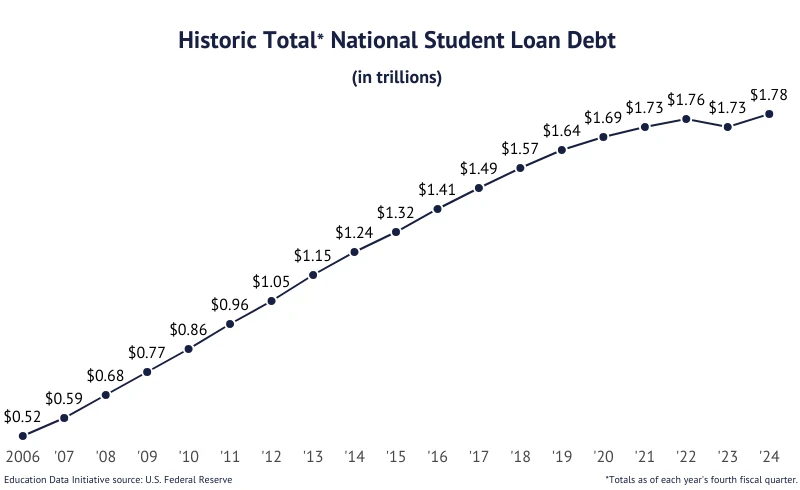

If you’ve ever whispered, “My student loan is ruining my life,” you’re far from alone. According to a recent year report by Education Data Initiative, U.S. student debt has climbed past $1.81 trillion, with millions of borrowers struggling to balance loan payments, rent, and basic needs.

Money expert Vivian Tu once said,

“You can’t manifest money—but you can reclaim control.”

And that’s what this guide is about — helping you take back your power, one informed and realistic step at a time.

In this blog, we’ll explore:

Student loans have reached a point where they’re not just numbers — they’re life sentences for many graduates. According to a 2024 report, federal student loans and private college debt are affecting more than 45 million borrowers across the U.S.

Rising interest rates and limited student loan forgiveness options have made repayment harder than ever. Many people are in the “horrible student loan in 2026” situation, where even after years of paying, the balance barely moves.

If you have student loans or need to apply for student loans with no cosigner, you’re not alone. These debts lead to higher interest rates and longer repayment timelines, leaving you stuck in survival mode.

Student loan systems differ drastically around the world. In countries like the U.K. or Germany, repayment is usually tied to income percentage, not fixed monthly payments. Borrowers pay only when they earn above a certain threshold — and many debts are forgiven after 25–30 years automatically.

In contrast, U.S. federal student loans require payments regardless of income, unless you specifically enroll in an income-driven repayment plan. This creates enormous pressure for low-earning graduates.

While Europe’s system isn’t perfect, it proves that student debt doesn’t have to crush their futures. It can adapt to income and circumstance. The U.S. can learn from these models by focusing on flexibility, fairness, and mental health impact when shaping future reforms.

Talking about numbers, I believe hearing real voices tells the story better.

YouTube: https://www.youtube.com/shorts/itTnxUf9GKg

One Reddit user shared:

“I graduated with a $140,000 student loan and a job that barely pays $45K a year. I feel like I’ll never get out.”

Another Instagram user was anxious about her 60K remaining loan.

She said:

''I’m unbelievably confused about what to do and if I can get married without destroying our budget for the next 25 years''

“I thought getting a degree meant security — now I’m scared to even check my balance.” (Quora User)

Please add here the attached screenshots as a gallery.

These stories are painfully common. Federal student loans were meant to open doors, but for many, they’ve become the reason those doors stay closed.

If you’ve ever thought, “My student loan is ruining my life,” know this: you’re not poor or lazy, and you’re not failing. The system was not built with today’s costs and wages in mind to manage student loans.

You can still take small, smart actions — like exploring

The goal isn’t perfection — it’s relief. And every little step toward stability counts. However, forgiveness doesn’t happen overnight. You may still need to stay consistent with payments or file additional documentation.

Student debt doesn’t just impact your wallet — it reshapes your entire life.

Debt can leave emotional scars: shame, burnout, and fear of planning for the future. But with time and strategy, you can shift from survival to rebuilding mode.

Many borrowers delay milestones such as marriage, buying a home, or even changing careers due to debt pressure.

I found Caleb Hammer, an influencer, evaluating the borrower’s problems here in his Live stream:

Link: https://www.youtube.com/watch?v=50Bj_6yoIp4

Here I see that it’s not just about money — it’s about lost freedom, postponed dreams, and constant stress.

On Instagram threads, I read this suggestion by a user, and it felt real to follow:

"I’m in the construction industry. For people with teenagers, I encourage kids to do trade school. Most come out with zero student debt, get to make money apprenticing while in school, and then get hired immediately after graduation with 2-4 years of experience on their resume.

People are retiring from trades in droves, so newly trained people will pretty much be able to name their salary. You don’t have to do manual labour either! I do complex construction sales and project management, and never touch a tool, but I’m clearing $500k in compensation this year and next year."

Start with a small, clear picture of your finances.

Sometimes the degree you chose doesn’t match the income you need — and that’s okay. Many graduates find that their dream major doesn’t support their dream lifestyle, especially when student loans are involved.

If your field isn’t paying enough, it might be time to consider a pivot into industries that are growing fast and hiring.

Blue-collar industries are one example. They may not sound glamorous, but they offer high income, job security, and room to grow. And you don’t have to do manual labor — these industries also need people in tech, design, administrative, operations, and marketing roles.

Another great option is the renewable energy sector. Solar, wind, and EV industries are expanding quickly and need workers in every area — from customer service to project coordination to technology support.

A pivot doesn’t mean giving up your dreams. It means aligning your skills with industries that can actually support your financial goals.

Like ($500–$1,000) to stay out of the credit card debt cycle. Money management isn’t about being rich — it’s about feeling in control again.

Debt stress is real. If you feel anxious, ashamed, or overwhelmed, you’re not weak — you’re human. Join a MentalHappy support group where you can connect with others navigating similar challenges. Sharing your story helps lighten the emotional weight.

Mindset matters — but it’s not a magic wand. As Vivian Tu (@YourRichBFF) says, “Menifesting money is a SCAM!” Positive thinking helps with motivation, but action is what changes your balance.

Check out what Vivian Tu is suggesting to get out of the situation and how to take things into your hands.

Even small steps can shift you from panic to progress:

Not everyone needs a four-year degree to succeed — and that’s a truth more young people are embracing. Rising tuition and college loans have pushed many to explore trade schools and apprenticeships as realistic, affordable options.

A 2025 report by EducationData.org shows that graduates of trade programs often start earning sooner and with 80% less debt than traditional college students. Careers in tech, healthcare, and skilled trades (like HVAC, coding bootcamps, or digital design) can provide solid income without lifelong financial pressure.

The message for future students is simple: education matters — but how you get it matters more. Explore every path before signing a loan document.

You’ve carried a heavy load, but you’re still standing — that counts for your resilience and mental strength. The road to financial recovery is not fast or straight. But it is possible.

You may have student loans, bad credit, or a long road ahead — but you’re no longer powerless. You’re learning, rebuilding, and choosing yourself again.

Your degree doesn’t define your debt — your resilience does. And that’s how you survive, grow, and start to thrive again in 2026.

You are not defined by your debt. Whether you’re managing federal student loans, dealing with bad credit, or simply trying to stay hopeful in 2026, remember this: progress doesn’t have to be fast to be real.

You’re already doing great by managing to survive — learning, adapting, and choosing to rebuild instead of giving up. Keep going!

You’re not behind — you’re becoming stronger, smarter, and freer, one payment and one choice at a time.

.svg)

.png)

.png)

.svg)

.svg)